During 2018 and 2019 the Trump administration put in place tariffs on approximately $380 billion of foreign products creating one of the largest tax increases of roughly $80 billion on Americans. The Biden administration has upheld these tariffs with minimal changes and has recently increased some as of May 14, 2024. This article will help to summarize the original tariffs put in place in 2018, discuss any updates or changes, and explain how these tariffs are impacting the manufacturing industry and next steps companies should take.

Section 201 - Washing Machines and Solar Panel

Washing Machines:

In 2018the Trump administration applied a safeguard tariff-rate quota on washing machines for three years and extended the tariff for another 2 years in 2021. As of February 7, 2023, the tariffs have expired and washers and covered parts are no longer eligible for quota entry types.

Solar Panels:

In 2018 The Trump Administration imposed tariffs on solar cells and modules for four years. The Biden administration extended the tariffs (excluding bifacial solar panels) for another 4 years in 2022 starting at 14.75% and decreasing .25% each year. Biden made a two-year exemption for some Southeast Asian countries that account for a large portion of solar panel imports.

Updates:

Biden recently announced that it will end the two-year delay of solar tariffs on southeast Asia and will not extend this exemption. Starting June 6, 2024, solar imports from Cambodia, Malaysia, Thailand, and Vietnam will be subject to tariffs again.

Solar cells were also included in the Biden administrations' Section 301 tariff increases as of May 14, 2024, which we will cover further in a later section.

Section 232 - Steel and Aluminum

A 25% tariff on imported steel and a 10% tariff on imported aluminum was imposed as of March 2018. However, many countries have been excluded from these tariffs over the years.

- Early on Australia was permanently excluded from the tariffs, while steel use quotas were agreed upon for South Korea and Brazil and an aluminum use quota for Argentina.

- Close behind in 2019 agreements were reached to drop these tariffs on Canada and Mexico while finalizing the US-Mexico-Canada Agreement on Trade.

- In 2022 Biden replaced the tariffs with tariff rate quota (TRQ) systems for certain countries including the European Union, Japan, and the UK for designated periods of time.

EU, Mexico, and China

European Union:

- The TRQ agreement with the European Union was set to expire this year January 2024, but Biden has extended this exemption for another two years until January 2026.

- The European Union in turn also extended the suspension of its rebalancing tariffs on US products in the context of the steel and aluminum dispute until March 31, 2025.

Mexico:

- Recent tensions have risen round the Mexico tariff exemption. The agreement made in 2019 hinged upon Mexico's agreement to be more transparent regarding steel and aluminum imports from third countries. A monitoring mechanism has shown increased imports from Mexico and the US believes the cheaper goods have been ultimately coming from China.

- The US has threatened reinstating tariffs on Mexico should this not be addressed. New legislation, Stop Mexico's Steel Surge Act, was introduced March 12, 2024, and is pushing for reinstating the 25% and 10% tariffs. Mexico has responded with threats of retaliatory tariffs of their own.

- On April 22, 2024, The Mexican government has established temporary import tariffs ranging from 5% to 50% for 544 HS codes including steel and aluminum. The tariffs are in effect from April 23, 2024, through April 23, 2026, and aims to combat unfair competition from countries with which Mexico doesn't have free trade agreements.

- The outcome of this dispute is still yet to be seen, but hopes are that both countries can come to an agreement without increasing tariffs.

China:

- Steel and aluminum were also included in the Biden administrations' Section 301 tariff increases as of May 14, 2024, which we will cover further in the next section.

Section 301 - Capital Goods from China

In 2018 the United States Trade Representative found in an investigation that China was conducting unfair trade practices regarding technology transfer, intellectual property, and innovation. The Trump Administration then proceeded to announce from 2018 to 2019 four stages of tariffs on capital goods from China.

- Stage 1: 25% tariff on $34 billion worth of Chinese imports started July 6, 2018

- Stage 2: 25% tariff on $16 billion worth of Chinese imports went into effect August 23, 2018

- Stage 3: 10% tariff on $200 billion worth of goods from China was imposed in September 2018. This rate increased to 25% in May 2019.

- Stage 4: Initially was scheduled as two parts: 4a covered a 15% tariff on $112 billion of imports starting September 1, 2019. This was later reduced to 7.5% in January 2020. 4b would be a continuation of the 15% tariff on another $160 billion of imports as of December 15, 2019. However, stage 4b was postponed indefinitely after reaching a trade deal with China in December 2019.

After these stages and exemptions were implemented, the United States is now imposing a 25 percent tariff on approximately $250 billion of imports from China and a 7.5 percent tariff on approximately $112 billion worth of imports from China. These numbers will now increase with the Biden Administrations' recent announcement.

Updates:

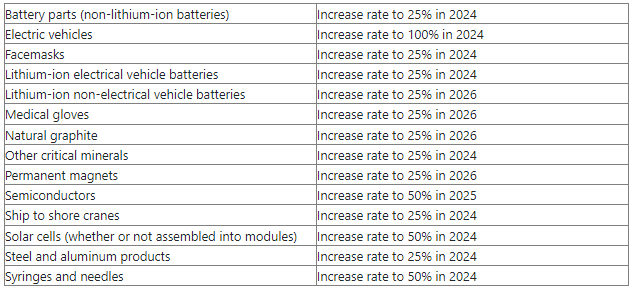

After completing the statutory four-year review of the Section 301 tariffs the Biden Administration has announced tariff increases on $18 billion of imports with a strong focus on clean energy and technology sectors. The manufacturing and medical industries will also see an impact. See below a full list of the tariff increases:

There are a few areas to make note of:

- The tariffs on Chinese Electric Vehicles have increased from 25% to 100% this year.

- Several items are increasing from 25% to 50% including solar cells and syringes and needles in 2024, and semiconductors in 2025.

- As mentioned earlier steel and aluminum will also be increasing to 25% this year.

While tariffs are meant to protect domestic industries from foreign competition to give them the time and opportunity to grow. However, results often show us tariffs have failed to boost the manufacturing industry and often produce higher costs for domestic consumers. Tariffs also typically give rise to retaliatory tariffs from other countries raising costs and inhibiting free trade and competition.

Scott Lincicome of the Cato Institute has illustrated how U.S. manufacturers face a competitive disadvantage due to the steel tariffs—the prices U.S. manufacturers pay for steel are significantly higher than what competitors in China, Europe, and elsewhere pay. The tariffs have also led to downstream job losses in the industry.

Similarly, the various solar panel tariffs have failed to make domestic production competitive, reduced investment, caused steep job losses, and reduced demand for solar panels by increasing the price. They also work against energy tax credits that promote investments in the solar industry, and overall hurts the goal of clean energy implementation.

Overall, it is estimated the tariffs in effect will reduce long-run GDP by 0.21 percent, wages by 0.14 percent, and employment by 166,000 full-time equivalent jobs.

Next Steps?

The best thing businesses in affected industries can do is closely monitor the changing landscape of international trade and evaluate how potential changes could affect their business through working with their customs brokers and trusted advisors. HLB Gross Collins MD&S industry practice will continue to monitor the dynamic tariffs environment and will provide updated articles with insights as new information arises.