MINIMIZING INDIVIDUAL TAXES

Income taxes

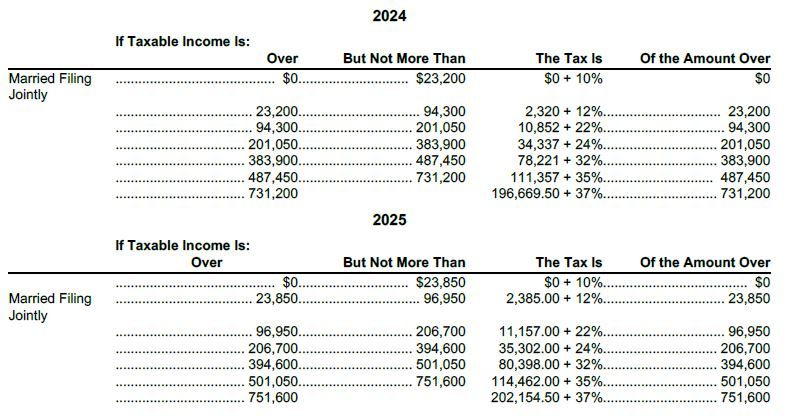

The key to any year-end planning strategy is to minimize taxes. This is generally done by either reducing the amount of income received or increasing the amount of deductions. With much uncertainty as to whether or not the TCJA will be extended or if the looming Fiscal Cliff will actually happen, planning for the next year can be overwhelming. However there is still time to implement tax planning strategies before the end of the year that can have a significant impact on your financial outlook. Given the proposals from the Trump campaign, lower taxes would likely apply to things that cannot be easily deferred (tip, Social Security, and overtime income). So, as in prior years, individual considerations are the most significant factor in play. The impact of inflation usually makes deferral of income a likely winner for almost all individuals. However, during the last year inflation has returned to a more familiar level from the historically high levels of inflation a couple years ago. In October, the IRS released the tax brackets for 2025. As an example of the increase in the brackets, the rates for married taxpayers filing jointly in 2024 compared to 2025 are below:

Individuals may not necessarily see increases in earnings that keep up with even that lower level of inflation, so if deferral of income from 2024 into 2025 is possible, it would mean that more income would fall into a lower tax bracket. In the long run, that would mean a lower aggregate tax burden.

Delaying and reducing gains.

Like taxes on ordinary income, taxes on capital gains also apply at different rates depending upon the amount of taxable income. For 2024, the rates are as follows:

For taxpayers whose income tends to fluctuate from year to year, it would be wise to examine the impact of sales of investment items. For taxpayers who think they may have lower income in 2025, it would be smart to hold off on a sale of a capital item if their income is at or near a threshold for a higher capital gains bracket. This type of consideration should not be limited to capital gain taxes, but also the net investment income (NII) tax. The 3.8% NII tax kicks in at $200,000 of modified adjusted gross income for single and head-of-household filers, $250,000 for joint filers, and $125,000 for married taxpayers filing separately.

A potential tax strategy involves selling investments at a loss to offset or reduce capital gains generated in the same tax year. However, the benefits only apply to high-income taxpayers. In addition, taxpayers must be mindful of the wash-sale rules that might disallow the loss if they reinvest in a 'substantially similar' asset within 30 days.

Maximizing deductions

For 2024, the inflation-adjusted standard deduction amounts are $29,200 for joint filers, $21,900 for heads of households, and $14,600 for all other filers. With standard deduction amounts so high, coupled with the $10,000 limitation on the deduction of state and local taxes, it is difficult for many taxpayers to claim enough deductions to make itemizing deductions beneficial. Thus, maximizing deductions may not be beneficial for all taxpayers. One of the best ways to maximize the amount of deductions is to develop a bunching strategy. This involves accumulating charitable contributions, or even medical expenses (see below), from two or more years into one year. For example, a taxpayer may have not made any of their normal charitable contributions in 2023, and then made double the normal amount in 2024 in order to help surpass the standard deduction amount. The same bunching strategy can be employed for deductible medical expenses where the timing is somewhat flexible, such as for elective procedures (remember that purely cosmetic procedures are not deductible).

Green energy

2023 was the first year that the Energy Efficiency Home Improvement Credit was available. The credit is generally equal to 30% of the taxpayer's qualified expenses, which can include doors, windows, other qualifying energy property, and even a home energy audit. Also available is the Residential Clean Energy Credit, which is also equal to 30% of qualified expenses. This credit is applicable to the installation of certain energy property like solar cells, small wind turbines, or battery storage. Restrictions and limitations do apply to both credits. The much more broadly applicable credit for the purchase of electric vehicles was eliminated upon the passage of the Inflation Reduction Act of 2022. In its place are two new credits, one $7,500 credit for the purchase of a new clean vehicle (with much more stringent requirements as compared to the old credit) and a $4,000 credit for the purchase of a used clean vehicle.

At the end of 2023, there wasn't much urgency in claiming these credits, but that may not necessarily be the case at the end of 2024. While the Trump campaign did not single out any specific credits, there was a general antipathy of many green energy initiatives. It is entirely possible that some or all of these green energy incentives could be on the chopping block to help pay for tax cuts elsewhere. If any action on this legislation in 2025

Retirement savings

Starting in 2023, the age at which required minimum distributions (RMDs) must begin is increased to 73 for individuals who turn 72 after 2022 and age 73 before 2033.

Remember that taxpayers who are in their first RMD year have until April 15 of the following year to make that first RMD. So, while action isn't absolutely necessary before the end of the year, affected taxpayers should start to plan for those RMDs. Keep in mind that the RMD for 2025 is required by December 31, 2025. If a taxpayer were to take both RMDs in 2025, it could push them into a higher tax bracket because both distributions would be taxable in one tax year. Qualified charitable distributions, or QCDs, offer eligible taxpayers aged 70 ½ or older a great way to easily give to charity before the end of the year. For those who are at least 72 years old, QCDs count toward the IRA owner's RMD for the year. QCDs are tax free if they are paid directly from the IRA to an eligible charitable organization. The annual limit for QCDs increases for the first time in 2024. The annual QCD limit is $105,000 (up from $100,000 in 2023).

SALT deduction

The Tax Cuts and Jobs Act (TCJA) capped the amount of the deduction for state and local taxes (SALT) at $10,000. Many legislators from higher-tax states have been clamoring for years to repeal or increase that limitation. While none of these efforts have proven successful so far, there is a strategy for taxpayers to claim this deduction that seems to have met with approval by the courts. Many states have enacted legislation that enables higher SALT deductions if paid by a passthrough entity. Requirements vary from state to state, so taxpayers looking to take advantage of this new strategy should speak with their tax professionals.

Other year-end strategies for individuals

A number of other traditional year-end strategies may apply. These include:

- Maximizing Education Credits - Individuals can claim a credit for tuition paid in 2024 even if the academic period begins in 2025, as long as the period begins by the end of March.

- Increasing 401(k) Contributions - Adjusted gross income (AGI) can be reduced if individuals increase the amount of their 401(k) contributions.

- IRA Contributions - Individuals eligible for deductions for IRA contributions can claim deductions, and thus reduce AGI, for amounts contributed generally through April 15, 2025.

- Teacher deductions - Educators can claim a deduction for up to $300 of classroom expenses (like books, supplies, and computer equipment, as well as personal protective equipment, disinfectant, and other supplies used to prevent the spread of COVID-19), and should maximize those expenses by year-end.